As artificial intelligence embeds itself deeper into the fabric of modern life, industries from healthcare to transportation are reconfiguring how they operate. But as machines take on tasks once reserved for humans-driving, diagnosing, even writing-the risk landscape is shifting dramatically, and insurers are being forced to catch up.

For every promise AI delivers-greater efficiency, faster decision-making, and cost savings-it brings a parallel stream of uncertainties. Who is accountable if a self-driving vehicle causes a crash? What happens when generative AI spreads misinformation, or when automated hiring tools discriminate unlawfully?

These are no longer hypothetical concerns. In recent years, algorithmic missteps have had real-world repercussions, from flawed COVID-19 diagnostic models to fatal accidents involving autonomous vehicles. A 2023 Stanford University report noted a staggering 2,500% surge in AI-related incidents and controversies since 2012.

Amid growing public scrutiny and regulatory attention, the insurance industry sees both a challenge and an opening. “While there will be exceptions,” said Dirk Hahn, CEO of the recruiting firm Hays, “the rise of AI could constrain the recovery in some junior white-collar roles.” The impacts of automation are already reshaping workforces, and insurers are working to understand where the liabilities lie.

In anticipation of a rising tide of AI-induced claims, several insurance giants and startups are moving into the space. Munich Re began offering targeted policies for AI developers as early as 2018, while Armilla AI now provides performance guarantees for machine learning models. These products aim to shield companies from risks such as biased outputs, intellectual property violations, and flawed model performance.

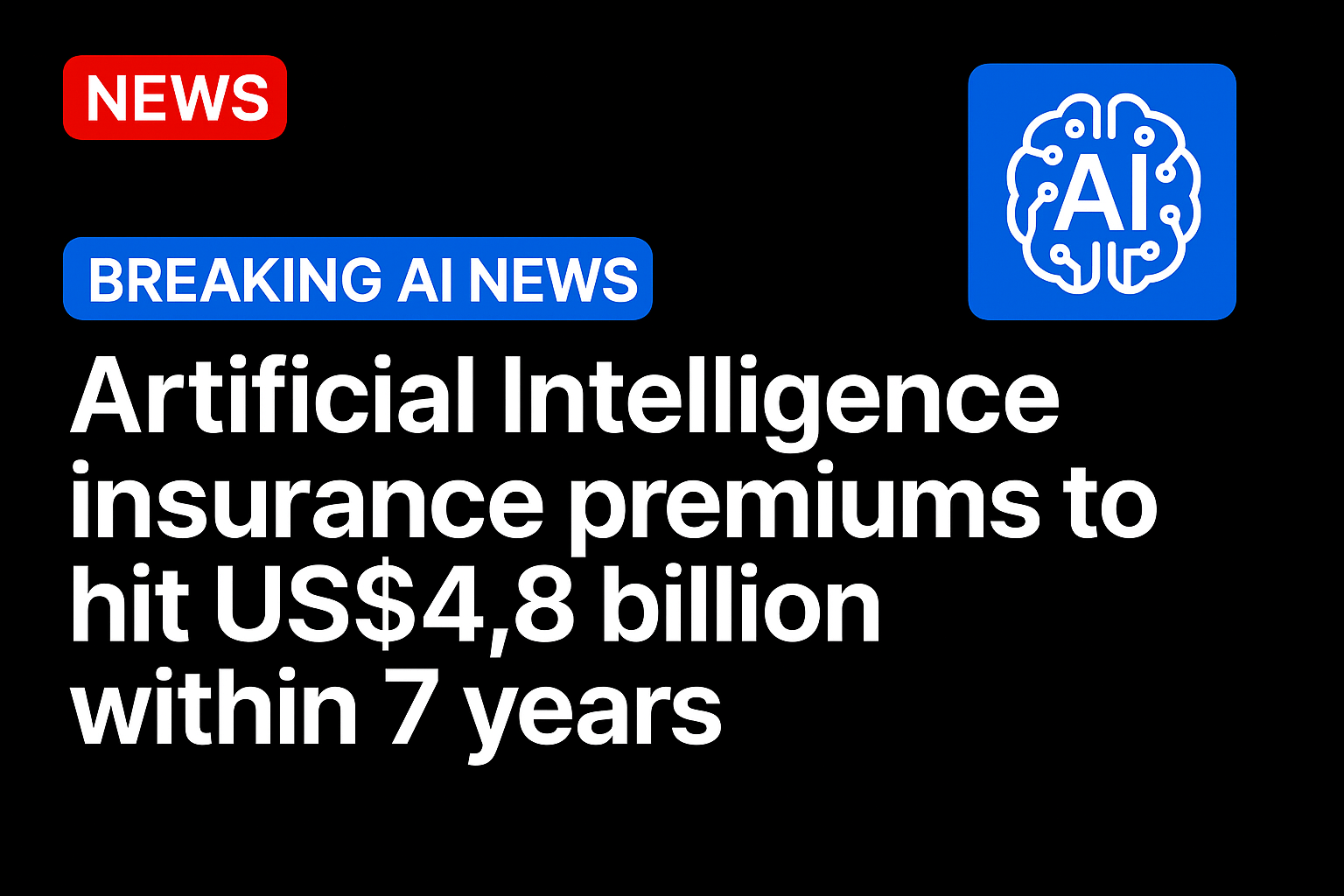

Estimates from the Deloitte Center for Financial Services suggest that this segment is poised for exponential growth. By 2032, global AI insurance premiums could top US$4.8 billion, expanding at an annual rate of roughly 80%.

To keep pace, insurers are developing bespoke assessment frameworks to price these emerging risks-no easy feat in a world where algorithms continuously evolve. The absence of reliable historical data only compounds the challenge. “As we learn, as we get more data, then we’ll figure out what the next steps are,” Jerry Gupta, head of AI & Insurance at Armilla told the Financial Times.

Policymakers are not waiting on the sidelines. The European Union is finalizing what would be the world’s most comprehensive regulatory regime for AI, including potential fines of up to US$38 million.

While these rules may not mandate insurance outright, they are likely to encourage it. As compliance costs rise and reputational risks mount, businesses are expected to turn to insurance to mitigate exposure.

This trend mirrors the evolution of cyber insurance. A few years ago, cyberattacks surged, prompting insurers to demand tighter risk controls and to introduce tailored policies. The same trajectory may now be unfolding in the AI domain.

For many companies, the allure of AI is hard to resist. From streamlining customer support to supercharging data analytics, the benefits are tangible. Microsoft, which recently posted a record-breaking market valuation of US$4 trillion, attributes much of its recent growth to AI. Yet it has also laid off thousands of workers-decisions explicitly linked to automation and efficiency gains.

The shift is cultural as much as it is technological. OpenAI CEO Sam Altman has floated the idea of one-person, billion-dollar companies. Even legacy firms are touting skeleton teams as a marker of innovation. One Big Four accounting firm, for example, reclaimed 3,600 analyst hours using AI-generated reports, slashing turnaround time for research by 75%.

But there are trade-offs. As AI becomes more embedded in daily operations, particularly in sectors like healthcare and finance, the cost of system failures or ethical lapses could be catastrophic.

In response, insurers are likely to take a cautious path forward, much as they did with cyber policies in the 2010s. Most will wait for clearer signals-more data, legal precedents, and the first wave of major claims-before they scale up.

In the meantime, carriers are leaning on AI audit firms and internal specialists to decode the often-opaque logic of machine learning systems. Understanding how these models make decisions-especially when those decisions impact lives or livelihoods-is essential before coverage terms can be standardized.

As AI accelerates, insurers face a familiar dilemma: whether to lead in shaping this frontier or to follow the first movers. One thing is clear-ignoring the risks is no longer an option. In a world where code increasingly acts in place of humans, the question is not whether AI will be insured, but how – and how soon.

Source: https://www.insurancebusinessmag.com/